Flash estimates launched by the City Redevelopment Authority (URA) and Housing and Improvement Board (HDB) on October 1 highlighted contrasting market performances within the third quarter of 2025. Non-public residence costs in Singapore rose for the fourth straight quarter in Q3 2025, pushed largely by a string of city-fringe and central launches. On the general public housing aspect, HDB resale costs continued to develop at a extra measured tempo, marking the slowest quarterly achieve in additional than 5 years.

Desk of contents

Non-public residential market: CCR leads progress

Non-public residence costs continued their regular climb in Q3 2025, rising 1.2% from the earlier quarter, in keeping with the URA’s flash estimates. This follows a 1.0% enhance in Q2 and brings total costs up by 3.1% to date this 12 months — practically double the expansion seen in the identical interval of 2024.

In Q3 2025, non-landed non-public houses costs climbed by 1.1% quarter-on-quarter (QoQ), accelerating from the 0.7% enhance within the earlier quarter. Right here’s how the completely different areas carried out inside the non-landed section:

- Core Central Area (CCR): Metropolis houses stole the highlight, with costs leaping 2.4%. This was the strongest progress throughout all areas, due to blockbuster launches like The Robertson Opus, UpperHouse at Orchard Boulevard, and River Inexperienced.

- Remainder of Central Area (RCR): Metropolis-fringe condos made a small comeback, ticking up 0.4% after slipping in Q2. Tasks like LyndenWoods and Promenade Peak helped carry gross sales and costs right here.

- Outdoors Central Area (OCR): Suburban condos held regular, including 1.0% in Q3 — nearly the identical tempo as final quarter. Reasonably priced mass-market launches akin to Springleaf Residence and Canberra Crescent Residences saved demand sturdy.

In the meantime, landed houses additionally stayed in demand, with costs up 1.4%. Indifferent homes led the cost, climbing 9% as extra consumers got here in. These embrace one big-ticket deal: a Good Class Bungalow at Chee Hoon Avenue offered for S$55 million.

With these regular beneficial properties, the non-public housing market appears to be like resilient, particularly with metropolis launches doing a lot of the heavy lifting. The ultimate Q3 figures might be confirmed on 24 October, however early indicators already level to sturdy purchaser confidence.

Huge launches energy CCR rebound

The standout story of Q3 was the rebound within the Core Central Area, due to a trio of main launches: The Robertson Opus, UpperHouse at Orchard Boulevard, and River Inexperienced. Collectively, they offered 835 new models, bringing total CCR new residence gross sales to about 900 models as of 21 September — the strongest quarterly exhibiting since This autumn 2010.

Learn extra: River Inexperienced units 2025 gross sales report for CCR

Within the RCR, gross sales have been anchored by LyndenWoods and Promenade Peak, every shifting 336 models. In the meantime, within the OCR, mass-market demand was strong. The 941-unit Springleaf Residence offered a powerful 883 models (94%) since its August launch, together with 92% snapped up on its first weekend. One other OCR mission, Canberra Crescent Residences, offered 233 out of 376 models (62%).

| Challenge | Area | Models Bought | Avg. Value (PSF) |

|---|---|---|---|

| Springleaf Residence | OCR | 883 | S$2,176 |

| River Inexperienced | CCR | 464 | S$3,120 |

| Promenade Peak | RCR | 336 | S$2,969 |

| LyndenWoods | RCR | 336 | S$2,462 |

| Canberra Crescent Residences | OCR | 233 | S$1,986 |

| UpperHouse | CCR | 202 | S$3,304 |

| The Robertson Opus | CCR | 169 | S$3,356 |

| Artisan 8 | RCR | 16 | S$2,388 |

| Whole | 2,639 |

By way of affordability, about 68% of recent non-landed non-public houses offered in Q3 2025 have been priced under S$2.5 million. The biggest share fell within the S$1.5 million to <S$2 million bracket (28.9%), adopted by S$2 million to <S$2.5 million (19.8%).

“Patrons are more and more targeted on worth, amenity, and comfort. Therefore, tasks which can be attractively priced and have sturdy transport hyperlinks will see extra strong demand, as seen in Springleaf Residence“, Kelvin Fong, CEO of PropNex, famous.

Learn extra: OCR new launches drove builders’ gross sales surge to 9-month excessive in August

Forecasts for the non-public market

Trying ahead, the momentum within the CCR is anticipated to proceed in This autumn. The upcoming Skye at Holland — the ultimate CCR launch of the 12 months — will provide 666 models, with 2-bedders ranging from about S$1.51 million and 3-bedders from S$2.40 million. Different This autumn launches, akin to Penrith (RCR), Faber Residence (OCR), and Zyon Grand (RCR) will additional widen purchaser choices.

See the complete listing of recent condominium launches in 2025 right here.

PropNex forecasts non-public residence costs might rise 4% to five% in 2025, near final 12 months’s 3.9% progress. Market help is anticipated from decrease rates of interest, sturdy upgrader demand, and the wholesome launch pipeline.

The easing rate of interest atmosphere is a key tailwind. The US Federal Reserve has minimize charges 4 occasions since March 2022, most just lately in September, and the 3-Month Compounded SORA in Singapore has dropped from 3.02% at the beginning of the 12 months to about 1.45% p.a. as of 1 October 2025.

HDB resale market: Slower value progress

On the HDB aspect, flash estimates present that resale costs continued to rise in Q3 2025, however at a a lot slower tempo. Costs edged up 0.4% from the earlier quarter, a a lot smaller enhance in comparison with the QoQ enhance of 0.9% in Q2.

That is now the fourth consecutive quarter of slowing progress, suggesting that the market is beginning to cool barely after two years of regular beneficial properties. Moreover, progress in Q3 2025 additionally represents the slowest quarterly rise in additional than 5 years — since Q2 2020, when costs inched up simply 0.3%.

By way of gross sales quantity, 7,157 flats modified arms in Q3 2025 (as much as 29 September), barely greater than the 7,102 transactions in Q2. This brings the full variety of resale flats offered within the first 9 months of the 12 months to twenty,849 models, in comparison with 22,562 models over the identical interval in 2024.

Thus far in 2025, resale costs have climbed by 2.9% over the primary 9 months, a way more average tempo in comparison with the 6.9% progress over the identical interval in 2024. Even so, resale costs are nonetheless at report highs, supported by ongoing demand from consumers preferring move-in-ready houses over ready for BTO flats.

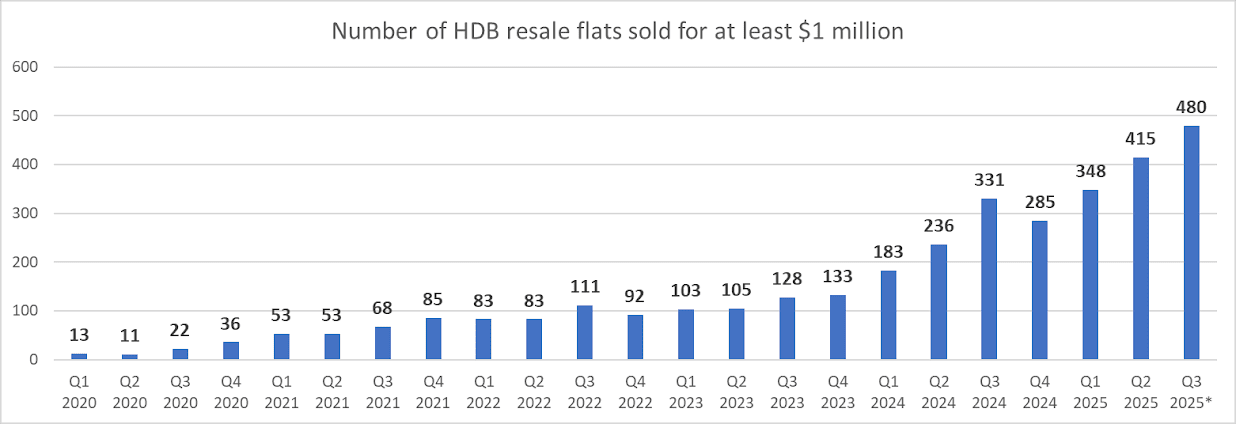

Extra million-dollar flats, regardless of easing value progress

Regardless of the worth moderation, million-dollar HDB offers stay a fixture. Q3 continued to see a gradual stream of record-setting transactions, notably in mature estates and uncommon flat varieties akin to massive government models or centrally positioned resale flats.

An estimated 480 resale flats have been offered for at the very least S$1 million in Q3 2025, up from 415 in Q2. That brings the 9M 2025 tally to 1,243 such flats, already surpassing the full-year report of 1,035 in 2024. These gross sales made up round 6% of all resale transactions within the first 9 months of this 12 months.

In accordance with PropNex, the million-dollar offers in Q3 2025 comprised one 3-room terrace, 204 4-room models, 172 5-room models, 102 government flats, and one multi-gen flat. Cities with the very best gross sales have been Toa Payoh (92 models), Bukit Merah (61 models), and Kallang Whampoa (40 models).

The persistence of million-dollar flats highlights the uneven nature of the market: whereas the general tempo of progress is slowing, fascinating models with distinctive attributes akin to measurement, location, or shortage, stay in excessive demand.

Outlook for the HDB resale market

The regular provide of recent flats by way of Construct-to-Order (BTO) and Sale of Steadiness Flats (SBF) launches helps to stabilise the market by giving consumers extra alternate options, particularly in a 12 months with comparatively few flats reaching their Minimal Occupation Interval (MOP). Solely 8,000 models will MOP in 2025, which limits resale inventory.

Learn extra: HDB BTO MOP 2025 & 2026 – Finest picks inside a 10-minute stroll to MRT & LRT stations

That mentioned, demand for well-located flats — particularly these close to MRT stations, in central cities, on excessive flooring, or with bigger layouts and longer leases — is anticipated to stay sturdy.

The federal government can be reviewing the family earnings ceiling for BTO purposes, which might shift some demand from resale flats again to new launches. This, along with the continued 15-month wait-out interval coverage, could hold total value progress average.

What it means for consumers and sellers

Q3 2025 painted a nuanced image of Singapore’s housing market. The non-public sector, led by the CCR, is exhibiting contemporary energy after a muted interval, whereas the HDB resale market is coming into a section of moderation. Collectively, they replicate a market that’s neither overheated nor collapsing, however slightly recalibrating to new realities of affordability, demand, and provide.

For consumers, the developments spotlight shifting affordability thresholds. HDB upgraders who as soon as appeared to the OCR for inexpensive entry into non-public housing are actually dealing with greater limitations, as OCR costs have inched up and new launches are priced above S$2,000 psf. In the meantime, wealthier consumers are gravitating again in the direction of CCR properties, that are perceived as relative bargains in comparison with international benchmarks.

The rest of 2025 will see a number of notable non-public launches, notably in central districts. This pipeline is more likely to maintain purchaser curiosity, although the market will stay delicate to pricing methods. Within the HDB section, upcoming October BTO workouts might additional ease strain on resale flats, providing extra selections for first-timers. That mentioned, sellers within the resale market could have to mood expectations. Whereas million-dollar offers stay doable, the pool of consumers keen to stretch budgets is anticipated to be smaller.

The put up Q3 2025 flash estimate: Non-public market resilience meets HDB value moderation appeared first on .