In a considerably stunning transfer, mortgage financier Freddie Mac is upping most loan-to-value ratios on 2-4 unit main residences.

The transfer comes amid a potential preliminary public providing for each Freddie Mac and Fannie Mae.

It’s unclear why the corporate is increasing eligibility for its mortgages, particularly on multi-unit properties, however we’ll discover some potential causes under.

Definitely attention-grabbing timing given the housing market’s struggles of late, with sky-high residence costs and equally steep mortgage charges hindering affordability.

Maybe this may result in extra residence buy demand whereas boosting market share for the corporate.

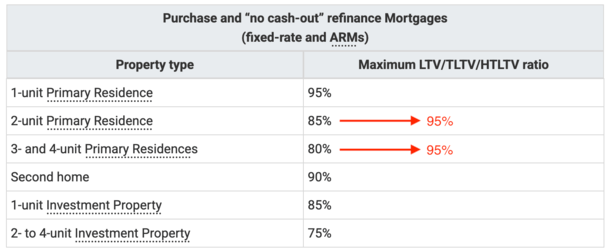

Max LTVs/CLTVs Upped to 95% for Multi-Unit Properties

As famous, you’ll quickly be capable to borrow as much as 95% LTV on a 2-4 unit property with a mortgage backed by Freddie Mac.

This consists of LTV/TLTV/HTLTV, which suggests you will get a second mortgage like a HELOC behind it as much as 95% as effectively.

The soar is fairly vital. It’s at the moment a most of 85% for a 2-unit property and 80% for a 3-4 unit property.

So we’re speaking a rise of 10% and 15%, respectively, at a time when residence costs are already arguably too excessive.

Particularly, the brand new most LTVs apply to main residences which might be 2-4 items, which means you need to occupy one of many items, a minimum of initially.

As well as, the mortgage have to be both a house buy mortgage or a charge and time period refinance (often called a “no cash-out” refinance).

It doesn’t apply to cash-out refinances, which stay at a extra restrictive 75% for a 2-4 unit main residence.

That’s a very good factor given the place we’re at within the housing cycle. We don’t need to go down the identical path of permitting owners to get overextended once more.

Whether or not this additional exacerbates the dearth of for-sale provide, or fills a necessity, stays to be seen.

However sometimes throughout instances when residence costs really feel a bit frothy, you may see corporations like Fannie Mae and Freddie Mac tighten their underwriting pointers.

For the document, Fannie Mae already allowed 95% LTVs for 2-4 unit main residences because of an October 2023 replace, so this aligns pointers between the pair.

On the time, Fannie mentioned the transfer was to “develop entry to credit score and supply help for reasonably priced rental housing.”

Why Are They Elevating LTVs When Housing Affordability Is Already a Drawback?

Given the place the housing market stands in the present day, with some drawing parallels to the GFC and mortgage disaster of the early 2000s, it’s a bit of unusual.

Usually lenders pull again after they’re involved debtors may be getting in over their heads.

Or if job safety turns into extra of a fear, this time because of rising expertise like AI and a potential recession.

For issues to go the opposite means makes you marvel what they’re as much as over at Freddie Mac.

Perhaps they’ve been dropping market share to non-agency lenders, particularly non-QM lenders.

This could possibly be a strategy to drum up enterprise, particularly as they plan to go public sooner or later within the close to future, and/or align pointers with Fannie Mae if the 2 by some means merge.

Eventually look, shares of Freddie Mac (OTCMKTS: FMCC) had been buying and selling at over $11 per share, up practically 20% in the present day and over 100% over the previous six months.

It’s fully potential that they’re increasing their product menu to compete with non-QM lenders and even FHA loans, which permit even greater LTVs as much as 96.5% on 2-4 unit properties.

Given the recognition of so-called home hacking, the place you reside in a single unit and lease the others, this is smart.

The new pointers go into impact on for mortgages with settlement dates on or after September twenty ninth, 2025.

Word that the up to date LTVs don’t apply to manually underwritten mortgages or tremendous conforming mortgages, the latter of that are reserved for borrower in high-cost markets.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence patrons higher navigate the house mortgage course of. Observe me on X for warm takes.

Defined")